The prior two posts (January 10 & December 20) covered where these commodity prices were in 2020 and where the futures prices of these commodities are going. The four commodity prices are largely determined by available inventories. When there is a lot available, prices will be lower than when commodities are scarce.

This post will examine the inventory levels and prices of cheese and butter over the last three years and where they currently stand. Because NDM and dry whey prices are determined by global inventories they will not be covered in this post. Cheese and butter prices are the main determinants of butterfat, milk protein, and Class III milk prices. NDM which is not covered in this post has a strong influence on the Producer Price Differential. Dry whey prices are used to set the price of Other Solids in milk and has a small influence on producer milk prices.

Monthly changes can be very volatile and therefore can be misleading and difficult to follow. The data in this post is based exclusively on twelve-month moving averages. Twelve-month averages decrease the volatility of seasonal and monthly swings and allow better visibility of where the market is and where it may be going.

In some of the charts below, there are “blips” in around March and April 2020. That is when the impact of COVID and the drastic shifts in consumer demand started. The changes were drastic, and it took a while for the production and supply chains to manage the changes. That time has passed, and those changes should be considered as a one-time event that has passed.

Data for 2020 is available through November 2020.

BUTTER

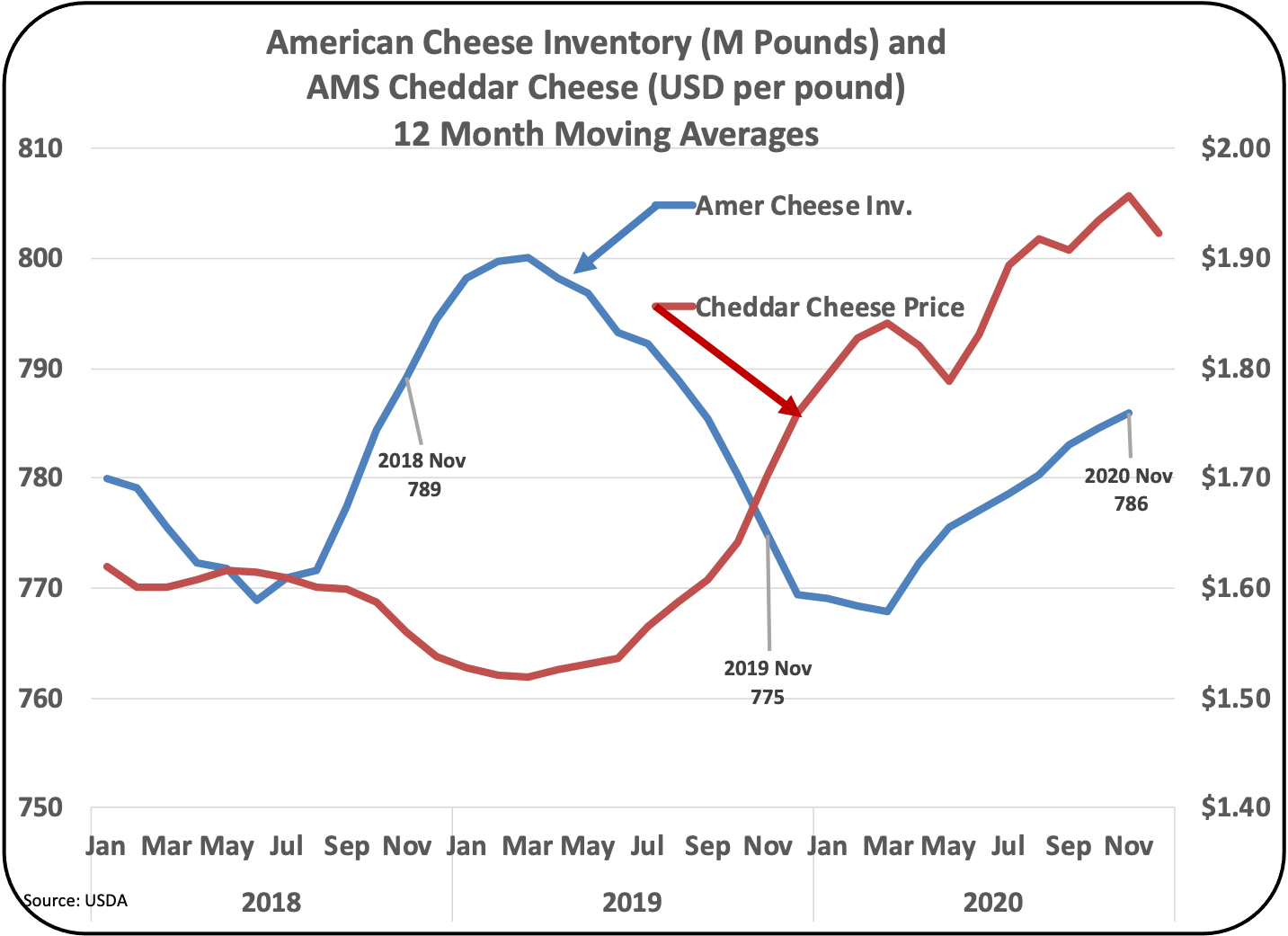

The price of butter determines the price that all Federal Milk Marketing Order producers get for butterfat. Therefore, the price of butter is very important. There is a inverse correlation between butter inventories and butter prices. In the last few years butter prices increased to record levels as inventories were tight. During 2020 the inventories levels increased, and butter prices dropped to more typical levels.

Chart I below provides a very clear view of the correlation between butter inventories and butter prices. During 2018 and 2019, inventories were very low and prices were high. In 2020, the inventories increased, and prices tumbled. The inverse relationship here is very clear.

|

| Chart I – Butter Inventories and Prices |

In turn, this begs the question as to why the inventories were low and what changed to increase the wholesale availability of butter. The answer to this is somewhat complex with multiple variables contributing to these inventory swings.

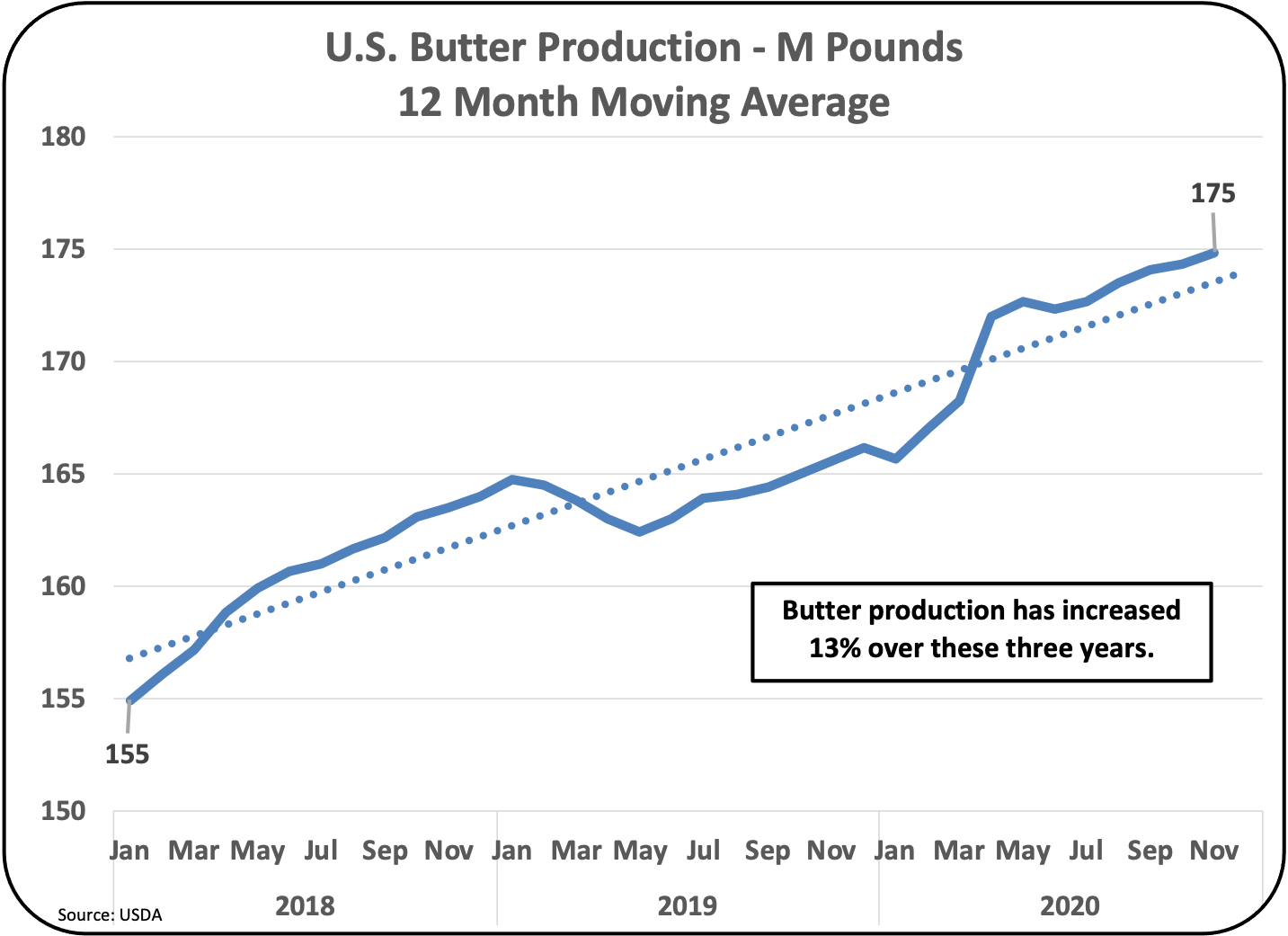

The first thing to be covered will be butter production (churning). Chart II illustrates the increase in butter production. Since the start of 2018 to the end of 2020, U.S. butter production has increased by 13 percent. This is well above the increases in domestic demand. Therefore, it resulted in an increase in inventories. Milk production of butterfat has continued to reach new record highs and new capacity for churning has also contributed to the increase in butter production.

|

| Chart II – Butter Production |

Chart III below repeats the above chart with domestic production of butter and adds a comparison to butter domestic disappearance from cold storage. Toward the end of 2020, the area in the circle on Chart III, shows the increasing spread of higher domestic production and a static level of domestic disappearance. Obviously, this will contribute to larger inventories. But this chart also shows that in 2018, production was well above disappearance. During that time, butter prices were still high, and inventories were low (Chart I). The answer to that is exports and imports that will be covered next.

|

| Chart III – Butter Production and Butter Disappearance |

Butter exports and imports have made some significant changes in 2018 through 2020. Butter exports (Chart IV) were high in 2018 and early 2019. This contributed to the low butter inventories and high prices in 2018 and early 2019.

|

| Chart IV – Butter Exports |

|

| Chart V – Butter Imports |

|

| Chart VI – Butter Net Exports |

|

| Chart VII – American Cheese Inventory and Pricing |

|

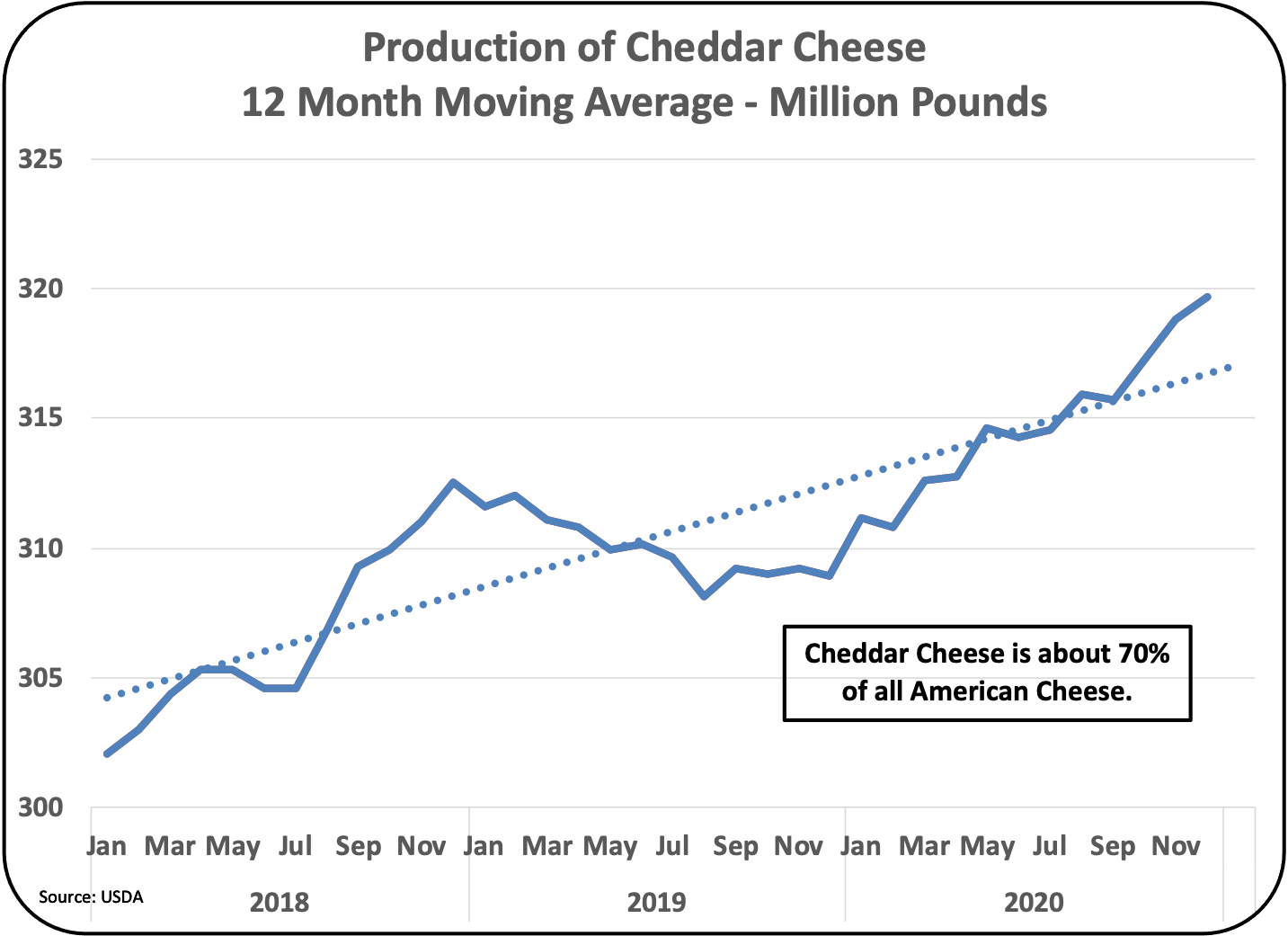

| Chart VIII – Production of Cheddar Cheese |

|

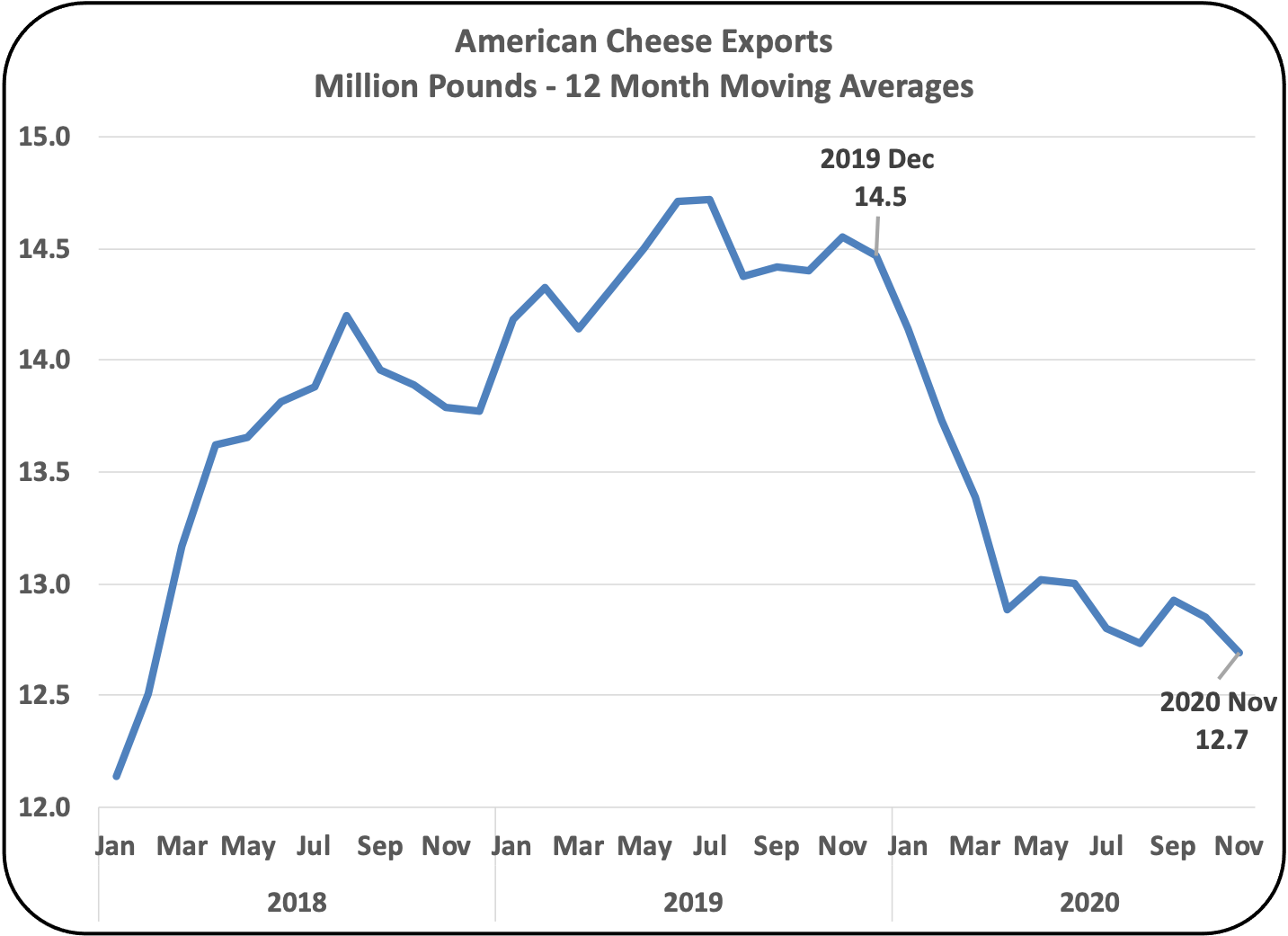

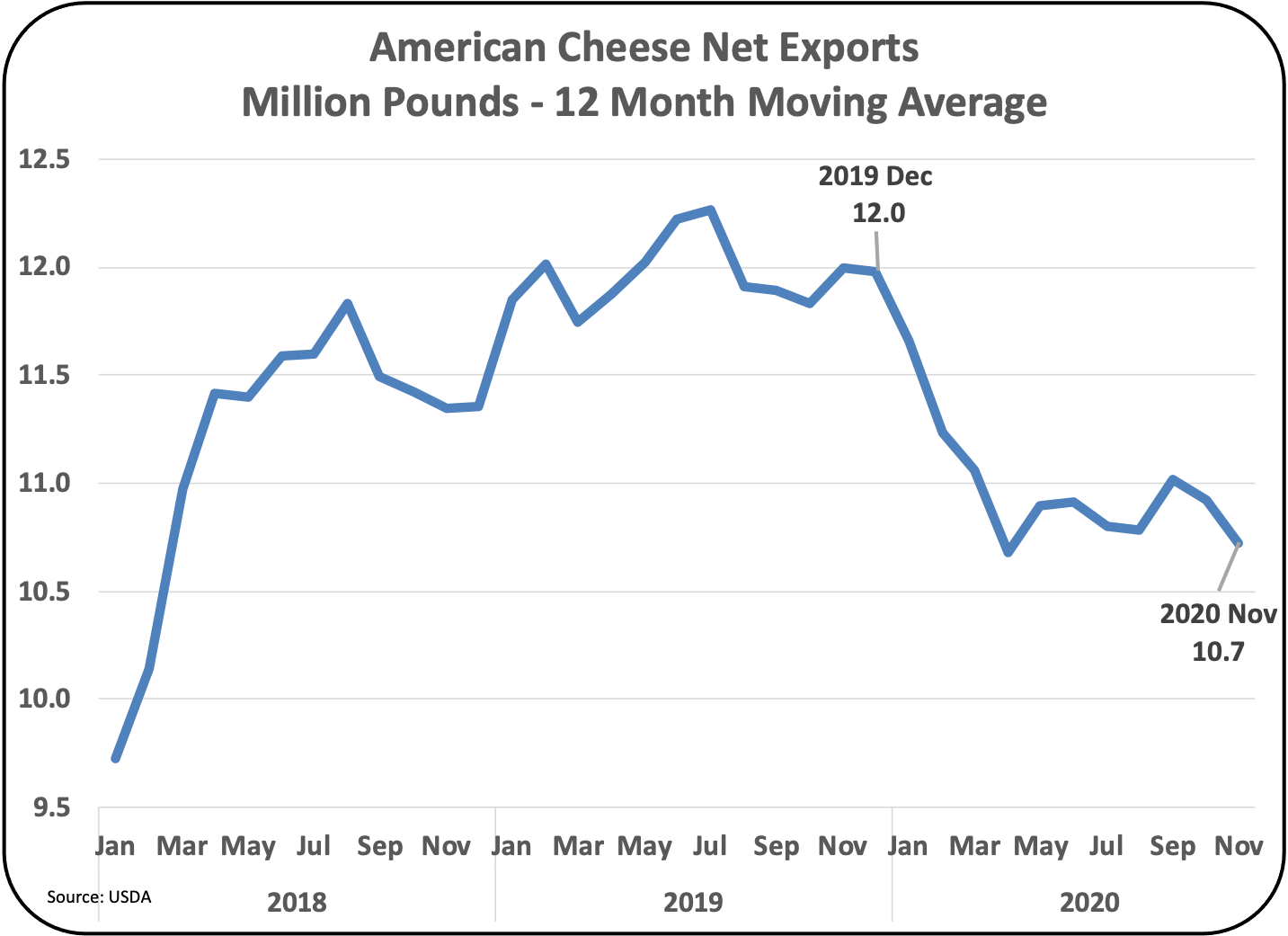

| Chart IX – Exports of American Cheese |

|

| Chart X – Net Exports of American Cheese |

|

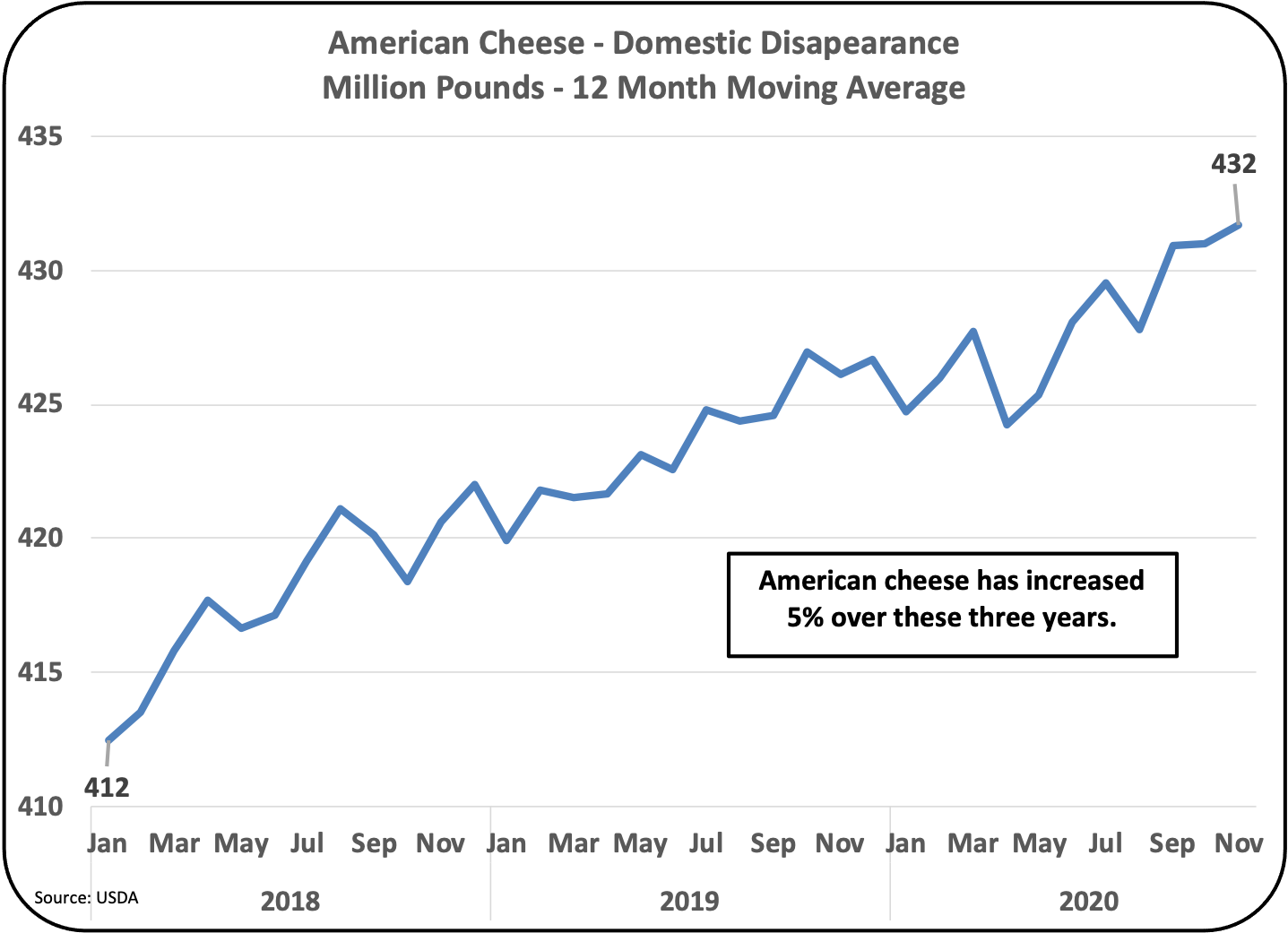

| Chart XI – American Cheese Domestic Disappearance |